Main Indicators @ MadnessCryptoInspired by veteran contributors of tradingview

Indicators list:

1. Main indicators: Moving average collection, Ichimoku, Bollinger Bands, fibonanci, simplize candlestick price action...

2. Price Action indicators: Candlesticks of (almost) any kinds. Harmonic Patterns: ABCD, Alt Bat, Butterfly, Crab, Wolf Wave, Head and Shoulders, Triangle...

3. Advanced indicators: top/bot finder, breakout detector, unpopular indicators

4. Signal & backtest tools: focus on two main factors: percent profitable & profit factor

Cheers,

Madness Crypto

-----------------------------------------------------------

Incase if those's scripts are useful, you can buy me a coffee

ETH & ERC20 tokens: 0xA2F57Cc46A5268F16A0224a81EDe7154218Ce890

Bitcoin: 1PTSbWK6snVSULBXhfx5TD9pJkkYCDe4PC

Binance & BEP2 tokens: bnb1tlxgpnguzq0w3w6myhd0t3d2j9wqd2pzpkudpc

חפש סקריפטים עבור "profit factor"

Ichimoku Clouds Strategy Long and ShortOverview:

The Ichimoku Clouds Strategy leverages the Ichimoku Kinko Hyo technique to offer traders a range of innovative features, enhancing market analysis and trading efficiency. This strategy is distinct in its combination of standard methodology and advanced customization, making it suitable for both novice and experienced traders.

Unique Features:

Enhanced Interpretation: The strategy introduces weak, neutral, and strong bullish/bearish signals, enabling detailed interpretation of the Ichimoku cloud and direct chart plotting.

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Dual Trading Modes: Long and Short modes are available, allowing alignment with market trends.

Flexible Risk Management: Offers three styles in each mode, combining fixed risk management with dynamic indicator states for versatile trade management.

Indicator Line Plotting: Enables plotting of Ichimoku indicator lines on the chart for visual decision-making support.

Methodology:

The strategy utilizes the standard Ichimoku Kinko Hyo model, interpreting indicator values with settings adjustable through a user-friendly menu. This approach is enhanced by TradingView's built-in strategy tester for customization and market selection.

Risk Management:

Our approach to risk management is dynamic and indicator-centric. With data from the last year, we focus on dynamic indicator states interpretations to mitigate manual setting causing human factor biases. Users still have the option to set a fixed stop loss and/or take profit per position using the corresponding parameters in settings, aligning with their risk tolerance.

Backtest Results:

Operating window: Date range of backtests is 2023.01.01 - 2024.01.04. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Maximum Single Position Loss: -6.29%

Maximum Single Profit: 22.32%

Net Profit: +10 901.95 USDT (+109.02%)

Total Trades: 119 (51.26% profitability)

Profit Factor: 1.775

Maximum Accumulated Loss: 4 185.37 USDT (-22.87%)

Average Profit per Trade: 91.67 USDT (+0.7%)

Average Trade Duration: 56 hours

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters. Backtest is calculated using deep backtest option in TradingView built-in strategy tester

How to Use:

Add the script to favorites for easy access.

Apply to the desired chart and timeframe (optimal performance observed on the 1H chart, ForEx or cryptocurrency top-10 coins with quote asset USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

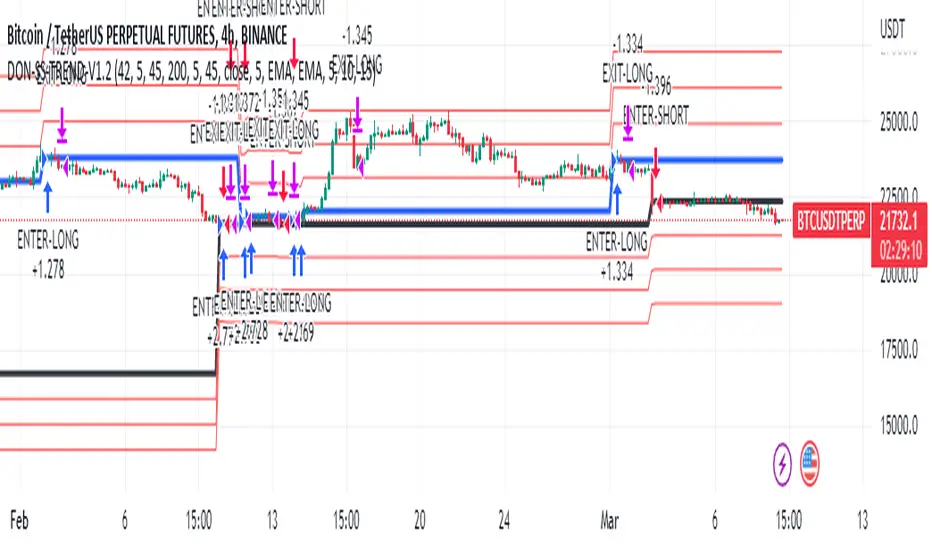

Donchian Trend V1The Donchian Trend strategy is a trend-following approach that uses the Donchian Channels indicator to identify potential entry and exit points in a security. The Donchian Channels are formed by taking the highest high and the lowest low prices over a specified period and plotting them as upper and lower channels around the current price. The width of the channels indicates the level of volatility in the market.

In this strategy, the Donchian Channels are used as a trend filter to determine the direction of the market. When the price is above the upper channel, it suggests an uptrend, and when the price is below the lower channel, it indicates a downtrend. The length of the Donchian Channels is a key parameter in the strategy, as it determines the look-back period for identifying the high and low prices.

Additional Logic: To further refine the entry and exit signals, The script uses two moving averages, a fast one (MA5) and a slow one (MA45), to identify trends and generate trading signals. When the fast moving average crosses above the slow moving average, a buy signal is generated, indicating that the market is trending upwards. Conversely, when the fast moving average crosses below the slow moving average, a sell signal is generated, indicating that the market is trending downwards.

Evaluation: The script was backtested on historical price data for the pair. The backtest results showed that the script was able to generate a net profit of , with a profit factor of and a Sharpe ratio of . The script also includes metrics such as the number of winning and losing trades, the average trade, and the largest winning and losing trades.

The strategy is evaluated based on its net profit, gross profit, gross loss, max run-up, max drawdown, buy & hold return, Sharpe ratio, Sortino ratio, and profit factor. The parameters used in the backtest include a Donchian Channel length of 42, which corresponds to a weekly time with divide of 4h time frame, and a short-term MA of 5 and a long-term MA of 45 for more accurate entry and exit signals.

Disclaimer: This script is for educational and research purposes only and should not be used for trading with real money without further testing and validation. Past performance is not indicative of future results.

KST Strategy [Skyrexio]Overview

KST Strategy leverages Know Sure Thing (KST) indicator in conjunction with the Williams Alligator and Moving average to obtain the high probability setups. KST is used for for having the high probability to enter in the direction of a current trend when momentum is rising, Alligator is used as a short term trend filter, while Moving average approximates the long term trend and allows trades only in its direction. Also strategy has the additional optional filter on Choppiness Index which does not allow trades if market is choppy, above the user-specified threshold. Strategy has the user specified take profit and stop-loss numbers, but multiplied by Average True Range (ATR) value on the moment when trade is open. The strategy opens only long trades.

Unique Features

ATR based stop-loss and take profit. Instead of fixed take profit and stop-loss percentage strategy utilizes user chosen numbers multiplied by ATR for its calculation.

Configurable Trading Periods. Users can tailor the strategy to specific market windows, adapting to different market conditions.

Optional Choppiness Index filter. Strategy allows to choose if it will use the filter trades with Choppiness Index and set up its threshold.

Methodology

The strategy opens long trade when the following price met the conditions:

Close price is above the Alligator's jaw line

Close price is above the filtering Moving average

KST line of Know Sure Thing indicator shall cross over its signal line (details in justification of methodology)

If the Choppiness Index filter is enabled its value shall be less than user defined threshold

When the long trade is executed algorithm defines the stop-loss level as the low minus user defined number, multiplied by ATR at the trade open candle. Also it defines take profit with close price plus user defined number, multiplied by ATR at the trade open candle. While trade is in progress, if high price on any candle above the calculated take profit level or low price is below the calculated stop loss level, trade is closed.

Strategy settings

In the inputs window user can setup the following strategy settings:

ATR Stop Loss (by default = 1.5, number of ATRs to calculate stop-loss level)

ATR Take Profit (by default = 3.5, number of ATRs to calculate take profit level)

Filter MA Type (by default = Least Squares MA, type of moving average which is used for filter MA)

Filter MA Length (by default = 200, length for filter MA calculation)

Enable Choppiness Index Filter (by default = true, setting to choose the optional filtering using Choppiness index)

Choppiness Index Threshold (by default = 50, Choppiness Index threshold, its value shall be below it to allow trades execution)

Choppiness Index Length (by default = 14, length used in Choppiness index calculation)

KST ROC Length #1 (by default = 10, value used in KST indicator calculation, more information in Justification of Methodology)

KST ROC Length #2 (by default = 15, value used in KST indicator calculation, more information in Justification of Methodology)

KST ROC Length #3 (by default = 20, value used in KST indicator calculation, more information in Justification of Methodology)

KST ROC Length #4 (by default = 30, value used in KST indicator calculation, more information in Justification of Methodology)

KST SMA Length #1 (by default = 10, value used in KST indicator calculation, more information in Justification of Methodology)

KST SMA Length #2 (by default = 10, value used in KST indicator calculation, more information in Justification of Methodology)

KST SMA Length #3 (by default = 10, value used in KST indicator calculation, more information in Justification of Methodology)

KST SMA Length #4 (by default = 15, value used in KST indicator calculation, more information in Justification of Methodology)

KST Signal Line Length (by default = 10, value used in KST indicator calculation, more information in Justification of Methodology)

User can choose the optimal parameters during backtesting on certain price chart.

Justification of Methodology

Before understanding why this particular combination of indicator has been chosen let's briefly explain what is KST, Williams Alligator, Moving Average, ATR and Choppiness Index.

The KST (Know Sure Thing) is a momentum oscillator developed by Martin Pring. It combines multiple Rate of Change (ROC) values, smoothed over different timeframes, to identify trend direction and momentum strength. First of all, what is ROC? ROC (Rate of Change) is a momentum indicator that measures the percentage change in price between the current price and the price a set number of periods ago.

ROC = 100 * (Current Price - Price N Periods Ago) / Price N Periods Ago

In our case N is the KST ROC Length inputs from settings, here we will calculate 4 different ROCs to obtain KST value:

KST = ROC1_smooth × 1 + ROC2_smooth × 2 + ROC3_smooth × 3 + ROC4_smooth × 4

ROC1 = ROC(close, KST ROC Length #1), smoothed by KST SMA Length #1,

ROC2 = ROC(close, KST ROC Length #2), smoothed by KST SMA Length #2,

ROC3 = ROC(close, KST ROC Length #3), smoothed by KST SMA Length #3,

ROC4 = ROC(close, KST ROC Length #4), smoothed by KST SMA Length #4

Also for this indicator the signal line is calculated:

Signal = SMA(KST, KST Signal Line Length)

When the KST line rises, it indicates increasing momentum and suggests that an upward trend may be developing. Conversely, when the KST line declines, it reflects weakening momentum and a potential downward trend. A crossover of the KST line above its signal line is considered a buy signal, while a crossover below the signal line is viewed as a sell signal. If the KST stays above zero, it indicates overall bullish momentum; if it remains below zero, it points to bearish momentum. The KST indicator smooths momentum across multiple timeframes, helping to reduce noise and provide clearer signals for medium- to long-term trends.

Next, let’s discuss the short-term trend filter, which combines the Williams Alligator and Williams Fractals. Williams Alligator

Developed by Bill Williams, the Alligator is a technical indicator that identifies trends and potential market reversals. It consists of three smoothed moving averages:

Jaw (Blue Line): The slowest of the three, based on a 13-period smoothed moving average shifted 8 bars ahead.

Teeth (Red Line): The medium-speed line, derived from an 8-period smoothed moving average shifted 5 bars forward.

Lips (Green Line): The fastest line, calculated using a 5-period smoothed moving average shifted 3 bars forward.

When the lines diverge and align in order, the "Alligator" is "awake," signaling a strong trend. When the lines overlap or intertwine, the "Alligator" is "asleep," indicating a range-bound or sideways market. This indicator helps traders determine when to enter or avoid trades.

The next indicator is Moving Average. It has a lot of different types which can be chosen to filter trades and the Least Squares MA is used by default settings. Let's briefly explain what is it.

The Least Squares Moving Average (LSMA) — also known as Linear Regression Moving Average — is a trend-following indicator that uses the least squares method to fit a straight line to the price data over a given period, then plots the value of that line at the most recent point. It draws the best-fitting straight line through the past N prices (using linear regression), and then takes the endpoint of that line as the value of the moving average for that bar. The LSMA aims to reduce lag and highlight the current trend more accurately than traditional moving averages like SMA or EMA.

Key Features:

It reacts faster to price changes than most moving averages.

It is smoother and less noisy than short-term EMAs.

It can be used to identify trend direction, momentum, and potential reversal points.

ATR (Average True Range) is a volatility indicator that measures how much an asset typically moves during a given period. It was introduced by J. Welles Wilder and is widely used to assess market volatility, not direction.

To calculate it first of all we need to get True Range (TR), this is the greatest value among:

High - Low

abs(High - Previous Close)

abs(Low - Previous Close)

ATR = MA(TR, n) , where n is number of periods for moving average, in our case equals 14.

ATR shows how much an asset moves on average per candle/bar. A higher ATR means more volatility; a lower ATR means a calmer market.

The Choppiness Index is a technical indicator that quantifies whether the market is trending or choppy (sideways). It doesn't indicate trend direction — only the strength or weakness of a trend. Higher Choppiness Index usually approximates the sideways market, while its low value tells us that there is a high probability of a trend.

Choppiness Index = 100 × log10(ΣATR(n) / (MaxHigh(n) - MinLow(n))) / log10(n)

where:

ΣATR(n) = sum of the Average True Range over n periods

MaxHigh(n) = highest high over n periods

MinLow(n) = lowest low over n periods

log10 = base-10 logarithm

Now let's understand how these indicators work in conjunction and why they were chosen for this strategy. KST indicator approximates current momentum, when it is rising and KST line crosses over the signal line there is high probability that short term trend is reversing to the upside and strategy allows to take part in this potential move. Alligator's jaw (blue) line is used as an approximation of a short term trend, taking trades only above it we want to avoid trading against trend to increase probability that long trade is going to be winning.

Almost the same for Moving Average, but it approximates the long term trend, this is just the additional filter. If we trade in the direction of the long term trend we increase probability that higher risk to reward trade will hit the take profit. Choppiness index is the optional filter, but if it turned on it is used for approximating if now market is in sideways or in trend. On the range bounded market the potential moves are restricted. We want to decrease probability opening trades in such condition avoiding trades if this index is above threshold value.

When trade is open script sets the stop loss and take profit targets. ATR approximates the current volatility, so we can make a decision when to exit a trade based on current market condition, it can increase the probability that strategy will avoid the excessive stop loss hits, but anyway user can setup how many ATRs to use as a stop loss and take profit target. As was said in the Methodology stop loss level is obtained by subtracting number of ATRs from trade opening candle low, while take profit by adding to this candle's close.

Backtest Results

Operating window: Date range of backtests is 2023.01.01 - 2025.05.01. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 60%

Maximum Single Position Loss: -5.53%

Maximum Single Profit: +8.35%

Net Profit: +5175.20 USDT (+51.75%)

Total Trades: 120 (56.67% win rate)

Profit Factor: 1.747

Maximum Accumulated Loss: 1039.89 USDT (-9.1%)

Average Profit per Trade: 43.13 USDT (+0.6%)

Average Trade Duration: 27 hours

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

How to Use

Add the script to favorites for easy access.

Apply to the desired timeframe and chart (optimal performance observed on 1h BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrexio commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation.

AlphaSync | QuantEdgeB📢 Introducing AlphaSync by QuantEdgeB

🛠️ Overview

AlphaSync is a comprehensive medium-term market guidance system designed for major assets such as BTC, ETH, and SOL. This system helps traders determine the overall market direction by integrating three universal strategies (EvolveXSync, ApexSync, QBHV Sync) and a Hybrid strategy (HybridSync).

🚀 What Makes AlphaSync Unique?

✅ Multi-Strategy Fusion → A robust blend of technical, economic, on-chain, and volatility-driven insights.

✅ HybridSync Component (90% Non-Price Factors) → Incorporates macro and liquidity signals to balance pure price-based models.

✅ Structured Decision-Making → The Trend Confluence score aggregates all sub-strategies, providing a unified market signal.

__________________________________________________________________________________

✨ Key Features

🔹 HybridSync (Hybrid Model)

Utilizes on-chain, economic, liquidity, and volatility factors to provide a fundamental market risk outlook. Unlike technical models, it derives signals primarily from macroeconomic indicators, risk appetite gauges, and capital flows.

🔹 EvolveXSync, & ApexSync (Technical Strategies)

Both strategies are purely price-based, relying on volatility-adjusted trend models, adaptive moving averages, and statistical deviations to confirm bullish or bearish trends.

🔹 QBHV Sync (Momentum & Deviation-Based System)

A fusion of momentum-deviation and a volatility-driven trend confirmation model, designed to detect shifts in momentum while filtering out market noise.

🔹 Trend Confluence (Final Aggregated Signal)

A weighted combination of all four models, delivering a single, structured signal to eliminate conflicting indicators and refine decision-making.

__________________________________________________________________________________

📊 How It Works

1️⃣ HybridSync – Non-Price Market Structure Analysis

HybridSync is an economic and liquidity-based framework, integrating macro variables, credit spreads, volatility indices, capital flows, and on-chain dynamics to assess risk-on/risk-off conditions.

📌 Key Components:

✔ On-Chain Metrics → Tracks investor behavior, exchange flows, and market cap ratios.

✔ Liquidity Indicators → Monitors global money supply (M2), Federal Reserve balance sheet, credit markets, and capital flows.

✔ Volatility & Risk Metrics → Uses MOVE, VIX, VVIX ratios, and bond market stress indicators to identify risk sentiment shifts.

🔹 Why HybridSync?

• Price alone does not dictate the market; macro liquidity and risk factors are often leading indicators of price movement, especially when it comes to risk assets such as cryptocurrencies.

• Improves decision-making in uncertain market environments, particularly during high-volatility or trendless conditions.

2️⃣ EvolveXSync, & ApexSync – Trend-Following & Volatility Models

Both EvolveXSync, & ApexSync are technical strategies, independently designed to capture trend strength and volatility dynamics.

📌 Core Mechanisms:

✔ VIDYA-Based Trend Detection → Adaptive moving averages adjust dynamically to price swings.

✔ SD-Filtered EMA Models → Uses normalized standard deviation levels to confirm trend validity.

✔ ATR-Adjusted Breakout Filters → Prevents false signals by incorporating dynamic volatility assessments.

🔹 Why Two UniStrategies?

• EvolveXSync, & ApexSync have different calculation methods, providing diverse perspectives on trend confirmation.

• Ensures robustness by mitigating overfitting to a single price-based model.

3️⃣ QBHV Sync – Momentum Deviation & Trend Confirmation

This component blends Bollinger Momentum Deviation (BMD) with a percentile-based trend model to confirm trend shifts.

📌 Core Components:

✔ Bollinger Momentum Deviation → A normalized SMA-SD filter detects overbought/oversold conditions.

✔ Percentile-Based Trend Confirmation → Ensures trends align with long-term volatility structure.

✔ Adaptive Signal Filtering → Prevents unnecessary trade signals by refining thresholds dynamically.

🔹 Why QBHV Sync?

• Adds a statistical layer to trend assessment, preventing whipsaws in volatile conditions.

• Complements HybridSync by ensuring price movements align with broader market forces.

4️⃣ Trend Confluence – The Final Aggregated Signal

AlphaSync blends HybridSync, EvolveXSync, ApexSync, and QBHV Sync into one final output.

📌 How It’s Weighted ? Equal Weight to remove any bias and over-reliance on one input.

✔ HybridSync (Macro & On-Chain Factors) → 25% Weight

✔ UniStrat V1 (Pure Trend) → 25% Weight

✔ UniStrat V2 (Trend + ATR) → 25% Weight

✔ QBHV Sync (Momentum & Deviation) → 25% Weight

🔹 Why Merge These Into One System?

The core philosophy behind AlphaSync is to create a holistic, structured decision-making framework that eliminates the weaknesses of single-method trading approaches. Instead of relying solely on technical indicators, which can lag or fail in macro-driven markets, AlphaSync blends price-based trend signals with macroeconomic, liquidity, and risk-adjusted models.

This multi-layered approach ensures that the system:

✔ Adapts dynamically to different market environments.

✔ Eliminates conflicting signals by creating a structured confluence score.

✔ Prevents over-reliance on a single market model, improving robustness.

📌 Final Signal Interpretation:

✅ Long Signal → AlphaSync Score > Long Threshold

❌ Short Signal → AlphaSync Score < Short Threshold

__________________________________________________________________________________

👥 Who Should Use AlphaSync?

✅ Medium-Term Traders & Portfolio Managers → Ideal for traders who require macro-confirmed trend signals.

✅ Systematic & Quantitative Traders → Designed for algorithmic integration and structured decision-making.

✅ Long-Term Position Traders → Helps identify major trend shifts and capital rotation opportunities.

✅ Risk-Conscious Investors → Incorporates macro volatility assessments to minimize unnecessary risk exposure.

__________________________________________________________________________________

📊 Backtest Mode - Evaluating Historical Performance

AlphaSync includes a fully integrated backtest module, allowing traders to assess its historical performance metrics.

🔹 Backtest Metrics Displayed:

✔ Equity Max Drawdown → Measures historical peak loss.

✔ Profit Factor → Evaluates profitability vs. loss ratio.

✔ Sharpe & Sortino Ratios → Risk-adjusted return metrics.

✔ Total Trades & Win Rate → Performance across different market cycles.

✔ Half Kelly Criterion → Optimal position sizing based on historical returns.

📌 Disclaimer:Backtest results are based on past performance and do not guarantee future success. Always incorporate real-time validation and risk management in live trading.

🚀 Why This Matters?

✅ Strategy Validation → See how AlphaSync performs across various market conditions.

✅ Customizable Analysis → Adjust parameters and observe real-time backtest results.

✅ Risk Awareness → Understand potential drawdowns before deploying capital.

Behavior Across Crypto Majors:

BTC

ETH

SOL

📌 Disclaimer: Backtest results are based on historical data and past market behavior. Performance is not indicative of future results and should not be considered financial advice. Always conduct your own backtests and research before making any investment decisions. 🚀

__________________________________________________________________________________

📌 Customization & Default Settings

📌 AlphaSync Input Parameters & Default Values

🔹 Strategy Configuration

• Color Mode → "Strategy"

• Extra Plots → true

• Long/Cash Signal Label → false

• AlphaSync Dashboard → true

• Enable BackTest Table → false

• Enable Equity Curve → false

• Table Position → "Bottom Left"

• Start Date → '01 Jan 2018 00:00'

• AlphaSync Long Threshold → 0.00

• AlphaSync Short Threshold → 0.00

🔹 QBHV.Sync

• DEMA Source → close

• DEMA Length → 14

• Percentile Length → 35

• ATR Length → 14

• Long Multiplier (ATR Up) → 1.8

• Short Multiplier (ATR Down) → 2.5

• Momentum Length → 8

• Momentum Source → close

• Base Length (SMA Calculation) → 40

• Source for BMD → close

• Standard Deviation Length → 30

• SD Multiplier → 0.7

• Long Threshold → 72

• Short Threshold → 59

🔹 EvolveXSync Configuration

• VIDYA Loop Length → 2

• VIDYA Loop Hist Length → 5

• Vidya Loop Long Threshold → 40

• Vidya Loop Short Threshold → 10

• Dynamic EMA Length → 12

• Dynamic EMA SD Length → 30

• Dynamic EMA Upper SD Weight → 1.032

• Dynamic EMA Lower SD Weight → 1.02

• SD Median Length → 12

• Normalized Median Length → 20

• Median SD Length → 30

• Median Long SD Weight → 0.98

• Median Short SD Weight → 1.04

🔹ApexSync Configuration

• DEMA Length → 30

• DEMA ATR Length → 14

• DEMA ATR Multiplier → 1.0

• G-VIDYA Length → 9

• G-VIDYA Hist Length → 30

• VIDYA ATR Length → 14

• VIDYA ATR Multiplier → 1.7

• SD Kijun Length → 24

• Normalized Kijun Length → 50

• KIJUN SD Length → 32

• KIJUN Long SD Weight → 0.98

• KIJUN Short SD Weight → 1.02

🔹 Risk Mosaic (Macro & Liquidity Component)

• Risk Signal Smoothing Length (EMA) → 8

🚀 AlphaSync is fully customizable to match different market conditions and trading styles

🚀 By default, AlphaSync is optimized for structured, medium-term market guidance.

__________________________________________________________________________________

📌 Conclusion

AlphaSync redefines medium-term trend analysis by merging technical, fundamental, and quantitative models into one unified system. Unlike traditional strategies that rely solely on price action, AlphaSync incorporates macroeconomic and liquidity factors, ensuring a more holistic market view.

🔹 Key Takeaways:

1️⃣ Hybrid + Technical Fusion – Balances macro & price-based strategies for stronger decision-making.

2️⃣ Multi-Factor Trend Aggregation – Reduces false signals by merging independent methodologies.

3️⃣ Structured, Data-Driven Approach – Designed for quantitative trading and risk-aware portfolio allocation.

📌 Master the market with precision and confidence | QuantEdgeB

🔹 Disclaimer: Past performance is not indicative of future results. No trading strategy can guarantee success in financial markets.

🔹 Strategic Advice: Always backtest, optimize, and align parameters with your trading objectives and risk tolerance before live trading.

[3Commas] Turtle StrategyTurtle Strategy

🔷 What it does: This indicator implements a modernized version of the Turtle Trading Strategy, designed for trend-following and automated trading with webhook integration. It identifies breakout opportunities using Donchian channels, providing entry and exit signals.

Channel 1: Detects short-term breakouts using the highest highs and lowest lows over a set period (default 20).

Channel 2: Acts as a confirmation filter by applying an offset to the same period, reducing false signals.

Exit Channel: Functions as a dynamic stop-loss (wait for candle close), adjusting based on market structure (default 10 periods).

Additionally, traders can enable a fixed Take Profit level, ensuring a systematic approach to profit-taking.

🔷 Who is it for:

Trend Traders: Those looking to capture long-term market moves.

Bot Users: Traders seeking to automate entries and exits with bot integration.

Rule-Based Traders: Operators who prefer a structured, systematic trading approach.

🔷 How does it work: The strategy generates buy and sell signals using a dual-channel confirmation system.

Long Entry: A buy signal is generated when the close price crosses above the previous high of Channel 1 and is confirmed by Channel 2.

Short Entry: A sell signal occurs when the close price falls below the previous low of Channel 1, with confirmation from Channel 2.

Exit Management: The Exit Channel acts as a trailing stop, dynamically adjusting to price movements. To exit the trade, wait for a full bar close.

Optional Take Profit (%): Closes trades at a predefined %.

🔷 Why it’s unique:

Modern Adaptation: Updates the classic Turtle Trading Strategy, with the possibility of using a second channel with an offset to filter the signals.

Dynamic Risk Management: Utilizes a trailing Exit Channel to help protect gains as trades move favorably.

Bot Integration: Automates trade execution through direct JSON signal communication with your DCA Bots.

🔷 Considerations Before Using the Indicator:

Market & Timeframe: Best suited for trending markets; higher timeframes (e.g., H4, D1) are recommended to minimize noise.

Sideways Markets: In choppy conditions, breakouts may lead to false signals—consider using additional filters.

Backtesting & Demo Testing: It is crucial to thoroughly backtest the strategy and run it on a demo account before risking real capital.

Parameter Adjustments: Ensure that commissions, slippage, and position sizes are set accurately to reflect real trading conditions.

🔷 STRATEGY PROPERTIES

Symbol: BINANCE:ETHUSDT (Spot).

Timeframe: 4h.

Test Period: All historical data available.

Initial Capital: 10000 USDT.

Order Size per Trade: 1% of Capital, you can use a higher value e.g. 5%, be cautious that the Max Drawdown does not exceed 10%, as it would indicate a very risky trading approach.

Commission: Binance commission 0.1%, adjust according to the exchange being used, lower numbers will generate unrealistic results. By using low values e.g. 5%, it allows us to adapt over time and check the functioning of the strategy.

Slippage: 5 ticks, for pairs with low liquidity or very large orders, this number should be increased as the order may not be filled at the desired level.

Margin for Long and Short Positions: 100%.

Indicator Settings: Default Configuration.

Period Channel 1: 20.

Period Channel 2: 20.

Period Channel 2 Offset: 20.

Period Exit: 10.

Take Profit %: Disable.

Strategy: Long & Short.

🔷 STRATEGY RESULTS

⚠️Remember, past results do not guarantee future performance.

Net Profit: +516.87 USDT (+5.17%).

Max Drawdown: -100.28 USDT (-0.95%).

Total Closed Trades: 281.

Percent Profitable: 40.21%.

Profit Factor: 1.704.

Average Trade: +1.84 USDT (+1.80%).

Average # Bars in Trades: 29.

🔷 How to Use It:

🔸 Adjust Settings:

Select your asset and timeframe suited for trend trading.

Adjust the periods for Channel 1, Channel 2, and the Exit Channel to align with the asset’s historical behavior. You can visualize these channels by going to the Style tab and enabling them.

For example, if you set Channel 2 to 40 with an offset of 40, signals will take longer to appear but will aim for a more defined trend.

Experiment with different values, a possible exit configuration is using 20 as well. Compare the results and adjust accordingly.

Enable the Take Profit (%) option if needed.

🔸Results Review:

It is important to check the Max Drawdown. This value should ideally not exceed 10% of your capital. Consider adjusting the trade size to ensure this threshold is not surpassed.

Remember to include the correct values for commission and slippage according to the symbol and exchange where you are conducting the tests. Otherwise, the results will not be realistic.

If you are satisfied with the results, you may consider automating your trades. However, it is strongly recommended to use a small amount of capital or a demo account to test proper execution before committing real funds.

🔸Create alerts to trigger the DCA Bot:

Verify Messages: Ensure the message matches the one specified by the DCA Bot.

Multi-Pair Configuration: For multi-pair setups, enable the option to add the symbol in the correct format.

Signal Settings: Enable the option to receive long or short signals (Entry | TP | SL), copy and paste the messages for the DCA Bots configured.

Alert Setup:

When creating an alert, set the condition to the indicator and choose "alert() function call only".

Enter any desired Alert Name.

Open the Notifications tab, enable Webhook URL, and paste the Webhook URL.

For more details, refer to the section: "How to use TradingView Custom Signals".

Finalize Alerts: Click Create, you're done! Alerts will now be sent automatically in the correct format.

🔷 INDICATOR SETTINGS

Period Channel 1: Period of highs and lows to trigger signals

Period Channel 2: Period of highs and lows to filter signals

Offset: Move Channel 2 to the right x bars to try to filter out the favorable signals.

Period Exit: It is the period of the Donchian channel that is used as trailing for the exits.

Strategy: Order Type direction in which trades are executed.

Take Profit %: When activated, the entered value will be used as the Take Profit in percentage from the entry price level.

Use Custom Test Period: When enabled signals only works in the selected time window. If disabled it will use all historical data available on the chart.

Test Start and End: Once the Custom Test Period is enabled, here you select the start and end date that you want to analyze.

Check Messages: Check Messages: Enable this option to review the messages that will be sent to the bot.

Entry | TP | SL: Enable this options to send Buy Entry, Take Profit (TP), and Stop Loss (SL) signals.

Deal Entry and Deal Exit: Copy and paste the message for the deal start signal and close order at Market Price of the DCA Bot. This is the message that will be sent with the alert to the Bot, you must verify that it is the same as the bot so that it can process properly.

DCA Bot Multi-Pair: You must activate it if you want to use the signals in a DCA Bot Multi-pair in the text box you must enter (using the correct format) the symbol in which you are creating the alert, you can check the format of each symbol when you create the bot.

👨🏻💻💭 We hope this tool helps enhance your trading. Your feedback is invaluable, so feel free to share any suggestions for improvements or new features you'd like to see implemented.

__

The information and publications within the 3Commas TradingView account are not meant to be and do not constitute financial, investment, trading, or other types of advice or recommendations supplied or endorsed by 3Commas and any of the parties acting on behalf of 3Commas, including its employees, contractors, ambassadors, etc.

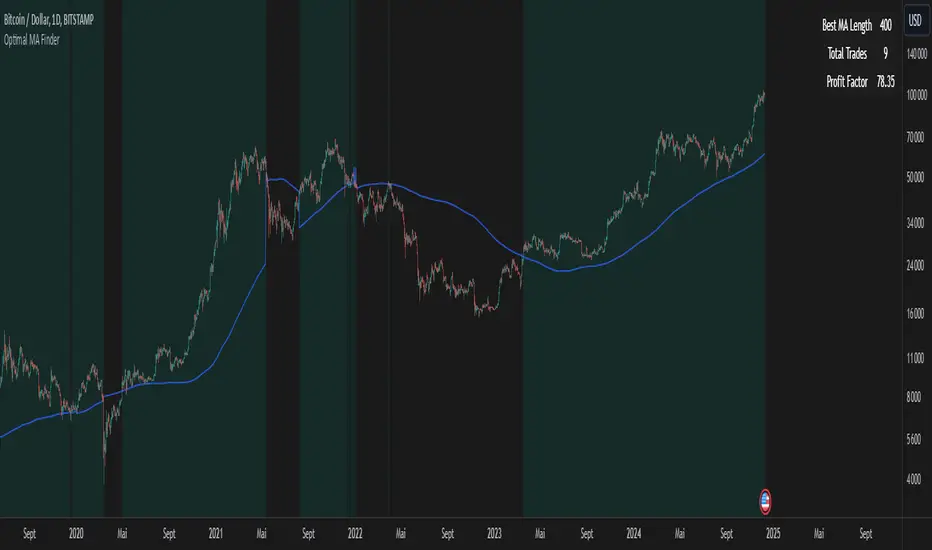

Optimal MA FinderIntroduction to the "Optimal MA Finder" Indicator

The "Optimal MA Finder" is a powerful and versatile tool designed to help traders optimize their moving average strategies. This script combines flexibility, precision, and automation to identify the most effective moving average (MA) length for your trading approach. Whether you're aiming to improve your long-only strategy or implement a buy-and-sell methodology, the "Optimal MA Finder" is your go-to solution for enhanced decision-making.

What Does It Do?

The script evaluates a wide range of moving average lengths, from 10 to 500, to determine which one produces the best results based on historical data. By calculating critical metrics such as the total number of trades and the profit factor for each MA length, it identifies the one that maximizes profitability. It supports both simple moving averages (SMA) and exponential moving averages (EMA), allowing you to tailor the analysis to your preferred method.

The logic works by backtesting each MA length against the price data and assessing the performance under two strategies:

Buy & Sell: Includes both long and short trades.

Long Only: Focuses solely on long positions for more conservative strategies.

Once the optimal MA length is identified, the script overlays it on the chart, highlighting periods when the price crosses over or under the optimal MA, helping traders identify potential entry and exit points.

Why Is It Useful?

This indicator stands out for its ability to automate a task that is often labor-intensive and subjective: finding the best MA length. By providing a clear, data-driven answer, it saves traders countless hours of manual testing while significantly enhancing the accuracy of their strategies. For example, instead of guessing whether a 50-period EMA is more effective than a 200-period SMA, the "Optimal MA Finder" will pinpoint the exact length and type of MA that has historically yielded the best results for your chosen strategy.

Key Benefits:

Precision: Identifies the MA length with the highest profit factor for maximum profitability.

Automation: Conducts thorough backtesting without manual effort.

Flexibility: Adapts to your preferred MA type (SMA or EMA) and trading strategy (Buy & Sell or Long Only).

Real-Time Feedback: Provides actionable insights by plotting the optimal MA directly on your chart and highlighting relevant trading periods.

Example of Use: Imagine you're trading a volatile stock and want to optimize your long-only strategy. By applying the "Optimal MA Finder," you discover that a 120-period EMA results in the highest profit factor. The indicator plots this EMA on your chart, showing you when to consider entering or exiting positions based on price movements relative to the EMA.

In short, the "Optimal MA Finder" empowers traders by delivering data-driven insights and improving the effectiveness of trading strategies. Its clear logic, combined with robust automation, makes it an invaluable tool for both novice and experienced traders seeking consistent results.

Optimized Heikin Ashi Strategy with Buy/Sell OptionsStrategy Name:

Optimized Heikin Ashi Strategy with Buy/Sell Options

Description:

The Optimized Heikin Ashi Strategy is a trend-following strategy designed to capitalize on market trends by utilizing the smoothness of Heikin Ashi candles. This strategy provides flexible options for trading, allowing users to choose between Buy Only (long-only), Sell Only (short-only), or using both in alternating conditions based on the Heikin Ashi candle signals. The strategy works on any market, but it performs especially well in markets where trends are prevalent, such as cryptocurrency or Forex.

This script offers customizable parameters for the backtest period, Heikin Ashi timeframe, stop loss, and take profit levels, allowing traders to optimize the strategy for their preferred markets or assets.

Key Features:

Trade Type Options:

Buy Only: Enter a long position when a green Heikin Ashi candle appears and exit when a red candle appears.

Sell Only: Enter a short position when a red Heikin Ashi candle appears and exit when a green candle appears.

Stop Loss and Take Profit:

Customizable stop loss and take profit percentages allow for flexible risk management.

The default stop loss is set to 2%, and the default take profit is set to 4%, maintaining a favorable risk/reward ratio.

Heikin Ashi Timeframe:

Traders can select the desired timeframe for Heikin Ashi candle calculation (e.g., 4-hour Heikin Ashi candles for a 1-hour chart).

The strategy smooths out price action and reduces noise, providing clearer signals for entry and exit.

Inputs:

Backtest Start Date / End Date: Specify the period for testing the strategy’s performance.

Heikin Ashi Timeframe: Select the timeframe for Heikin Ashi candle generation. A higher timeframe helps smooth the trend, which is beneficial for trading lower timeframes.

Stop Loss (in %) and Take Profit (in %): Enable or disable stop loss and take profit, and adjust the levels based on market conditions.

Trade Type: Choose between Buy Only or Sell Only based on your market outlook and strategy preference.

Strategy Performance:

In testing with BTC/USD, this strategy performed well in a 4-hour Heikin Ashi timeframe applied on a 1-hour chart over a period from January 1, 2024, to September 12, 2024. The results were as follows:

Initial Capital: 1 USD

Order Size: 100% of equity

Net Profit: +30.74 USD (3,073.52% return)

Percent Profitable: 78.28% of trades were winners.

Profit Factor: 15.825, indicating that the strategy's profitable trades far outweighed its losses.

Max Drawdown: 4.21%, showing low risk exposure relative to the large profit potential.

This strategy is ideal for both beginner and advanced traders who are looking to follow trends and avoid market noise by using Heikin Ashi candles. It is also well-suited for traders who prefer automated risk management through the use of stop loss and take profit levels.

Recommended Use:

Best Markets: This strategy works well on trending markets like cryptocurrency, Forex, or indices.

Timeframes: Works best when applied to lower timeframes (e.g., 1-hour chart) with a higher Heikin Ashi timeframe (e.g., 4-hour candles) to smooth out price action.

Leverage: The strategy performs well with leverage, but users should consider using 2x to 3x leverage to avoid excessive risk and potential liquidation. The strategy's low drawdown allows for moderate leverage use while maintaining risk control.

Customization: Traders can adjust the stop loss and take profit percentages based on their risk appetite and market conditions. A default setting of a 2% stop loss and 4% take profit provides a balanced risk/reward ratio.

Notes:

Risk Management: Traders should enable stop loss and take profit settings to maintain effective risk management and prevent large drawdowns during volatile market conditions.

Optimization: This strategy can be further optimized by adjusting the Heikin Ashi timeframe and risk parameters based on specific market conditions and assets.

Backtesting: The built-in backtesting functionality allows traders to test the strategy across different market conditions and historical data to ensure robustness before applying it to live trading.

How to Apply:

Select your preferred market and chart.

Choose the appropriate Heikin Ashi timeframe based on the chart's timeframe. (e.g., use 4-hour Heikin Ashi candles for 1-hour chart trends).

Adjust stop loss and take profit based on your risk management preference.

Run backtesting to evaluate its performance before applying it in live trading.

This strategy can be further modified and optimized based on personal trading style and market conditions. It’s important to monitor performance regularly and adjust settings as needed to align with market behavior.

RSI Trend Following StrategyOverview

The RSI Trend Following Strategy utilizes Relative Strength Index (RSI) to enter the trade for the potential trend continuation. It uses Stochastic indicator to check is the price is not in overbought territory and the MACD to measure the current price momentum. Moreover, it uses the 200-period EMA to filter the counter trend trades with the higher probability. The strategy opens only long trades.

Unique Features

Dynamic stop-loss system: Instead of fixed stop-loss level strategy utilizes average true range (ATR) multiplied by user given number subtracted from the position entry price as a dynamic stop loss level.

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Two layers trade filtering system: Strategy utilizes MACD and Stochastic indicators measure the current momentum and overbought condition and use 200-period EMA to filter trades against major trend.

Trailing take profit level: After reaching the trailing profit activation level script activates the trailing of long trade using EMA. More information in methodology.

Wide opportunities for strategy optimization: Flexible strategy settings allows users to optimize the strategy entries and exits for chosen trading pair and time frame.

Methodology

The strategy opens long trade when the following price met the conditions:

RSI is above 50 level.

MACD line shall be above the signal line

Both lines of Stochastic shall be not higher than 80 (overbought territory)

Candle’s low shall be above the 200 period EMA

When long trade is executed, strategy set the stop-loss level at the price ATR multiplied by user-given value below the entry price. This level is recalculated on every next candle close, adjusting to the current market volatility.

At the same time strategy set up the trailing stop validation level. When the price crosses the level equals entry price plus ATR multiplied by user-given value script starts to trail the price with trailing EMA(by default = 20 period). If price closes below EMA long trade is closed. When the trailing starts, script prints the label “Trailing Activated”.

Strategy settings

In the inputs window user can setup the following strategy settings:

ATR Stop Loss (by default = 1.75)

ATR Trailing Profit Activation Level (by default = 2.25)

MACD Fast Length (by default = 12, period of averaging fast MACD line)

MACD Fast Length (by default = 26, period of averaging slow MACD line)

MACD Signal Smoothing (by default = 9, period of smoothing MACD signal line)

Oscillator MA Type (by default = EMA, available options: SMA, EMA)

Signal Line MA Type (by default = EMA, available options: SMA, EMA)

RSI Length (by default = 14, period for RSI calculation)

Trailing EMA Length (by default = 20, period for EMA, which shall be broken close the trade after trailing profit activation)

Justification of Methodology

This trading strategy is designed to leverage a combination of technical indicators—Relative Strength Index (RSI), Moving Average Convergence Divergence (MACD), Stochastic Oscillator, and the 200-period Exponential Moving Average (EMA)—to determine optimal entry points for long trades. Additionally, the strategy uses the Average True Range (ATR) for dynamic risk management to adapt to varying market conditions. Let's look in details for which purpose each indicator is used for and why it is used in this combination.

Relative Strength Index (RSI) is a momentum indicator used in technical analysis to measure the speed and change of price movements in a financial market. It helps traders identify whether an asset is potentially overbought (overvalued) or oversold (undervalued), which can indicate a potential reversal or continuation of the current trend.

How RSI Works? RSI tracks the strength of recent price changes. It compares the average gains and losses over a specific period (usually 14 periods) to assess the momentum of an asset. Average gain is the average of all positive price changes over the chosen period. It reflects how much the price has typically increased during upward movements. Average loss is the average of all negative price changes over the same period. It reflects how much the price has typically decreased during downward movements.

RSI calculates these average gains and losses and compares them to create a value between 0 and 100. If the RSI value is above 70, the asset is generally considered overbought, meaning it might be due for a price correction or reversal downward. Conversely, if the RSI value is below 30, the asset is considered oversold, suggesting it could be poised for an upward reversal or recovery. RSI is a useful tool for traders to determine market conditions and make informed decisions about entering or exiting trades based on the perceived strength or weakness of an asset's price movements.

This strategy uses RSI as a short-term trend approximation. If RSI crosses over 50 it means that there is a high probability of short-term trend change from downtrend to uptrend. Therefore RSI above 50 is our first trend filter to look for a long position.

The MACD (Moving Average Convergence Divergence) is a popular momentum and trend-following indicator used in technical analysis. It helps traders identify changes in the strength, direction, momentum, and duration of a trend in an asset's price.

The MACD consists of three components:

MACD Line: This is the difference between a short-term Exponential Moving Average (EMA) and a long-term EMA, typically calculated as: MACD Line = 12 period EMA − 26 period EMA

Signal Line: This is a 9-period EMA of the MACD Line, which helps to identify buy or sell signals. When the MACD Line crosses above the Signal Line, it can be a bullish signal (suggesting a buy); when it crosses below, it can be a bearish signal (suggesting a sell).

Histogram: The histogram shows the difference between the MACD Line and the Signal Line, visually representing the momentum of the trend. Positive histogram values indicate increasing bullish momentum, while negative values indicate increasing bearish momentum.

This strategy uses MACD as a second short-term trend filter. When MACD line crossed over the signal line there is a high probability that uptrend has been started. Therefore MACD line above signal line is our additional short-term trend filter. In conjunction with RSI it decreases probability of following false trend change signals.

The Stochastic Indicator is a momentum oscillator that compares a security's closing price to its price range over a specific period. It's used to identify overbought and oversold conditions. The indicator ranges from 0 to 100, with readings above 80 indicating overbought conditions and readings below 20 indicating oversold conditions.

It consists of two lines:

%K: The main line, calculated using the formula (CurrentClose−LowestLow)/(HighestHigh−LowestLow)×100 . Highest and lowest price taken for 14 periods.

%D: A smoothed moving average of %K, often used as a signal line.

This strategy uses stochastic to define the overbought conditions. The logic here is the following: we want to avoid long trades in the overbought territory, because when indicator reaches it there is a high probability that the potential move is gonna be restricted.

The 200-period EMA is a widely recognized indicator for identifying the long-term trend direction. The strategy only trades in the direction of this primary trend to increase the probability of successful trades. For instance, when the price is above the 200 EMA, only long trades are considered, aligning with the overarching trend direction.

Therefore, strategy uses combination of RSI and MACD to increase the probability that price now is in short-term uptrend, Stochastic helps to avoid the trades in the overbought (>80) territory. To increase the probability of opening long trades in the direction of a main trend and avoid local bounces we use 200 period EMA.

ATR is used to adjust the strategy risk management to the current market volatility. If volatility is low, we don’t need the large stop loss to understand the there is a high probability that we made a mistake opening the trade. User can setup the settings ATR Stop Loss and ATR Trailing Profit Activation Level to realize his own risk to reward preferences, but the unique feature of a strategy is that after reaching trailing profit activation level strategy is trying to follow the trend until it is likely to be finished instead of using fixed risk management settings. It allows sometimes to be involved in the large movements.

Backtest Results

Operating window: Date range of backtests is 2023.01.01 - 2024.08.01. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 30%

Maximum Single Position Loss: -3.94%

Maximum Single Profit: +15.78%

Net Profit: +1359.21 USDT (+13.59%)

Total Trades: 111 (36.04% win rate)

Profit Factor: 1.413

Maximum Accumulated Loss: 625.02 USDT (-5.85%)

Average Profit per Trade: 12.25 USDT (+0.40%)

Average Trade Duration: 40 hours

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

How to Use

Add the script to favorites for easy access.

Apply to the desired timeframe and chart (optimal performance observed on 2h BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

MACD with 1D Stochastic Confirmation Reversal StrategyOverview

The MACD with 1D Stochastic Confirmation Reversal Strategy utilizes MACD indicator in conjunction with 1 day timeframe Stochastic indicators to obtain the high probability short-term trend reversal signals. The main idea is to wait until MACD line crosses up it’s signal line, at the same time Stochastic indicator on 1D time frame shall show the uptrend (will be discussed in methodology) and not to be in the oversold territory. Strategy works on time frames from 30 min to 4 hours and opens only long trades.

Unique Features

Dynamic stop-loss system: Instead of fixed stop-loss level strategy utilizes average true range (ATR) multiplied by user given number subtracted from the position entry price as a dynamic stop loss level.

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Higher time frame confirmation: Strategy utilizes 1D Stochastic to establish the major trend and confirm the local reversals with the higher probability.

Trailing take profit level: After reaching the trailing profit activation level scrip activate the trailing of long trade using EMA. More information in methodology.

Methodology

The strategy opens long trade when the following price met the conditions:

MACD line of MACD indicator shall cross over the signal line of MACD indicator.

1D time frame Stochastic’s K line shall be above the D line.

1D time frame Stochastic’s K line value shall be below 80 (not overbought)

When long trade is executed, strategy set the stop-loss level at the price ATR multiplied by user-given value below the entry price. This level is recalculated on every next candle close, adjusting to the current market volatility.

At the same time strategy set up the trailing stop validation level. When the price crosses the level equals entry price plus ATR multiplied by user-given value script starts to trail the price with EMA. If price closes below EMA long trade is closed. When the trailing starts, script prints the label “Trailing Activated”.

Strategy settings

In the inputs window user can setup the following strategy settings:

ATR Stop Loss (by default = 3.25, value multiplied by ATR to be subtracted from position entry price to setup stop loss)

ATR Trailing Profit Activation Level (by default = 4.25, value multiplied by ATR to be added to position entry price to setup trailing profit activation level)

Trailing EMA Length (by default = 20, period for EMA, when price reached trailing profit activation level EMA will stop out of position if price closes below it)

User can choose the optimal parameters during backtesting on certain price chart, in our example we use default settings.

Justification of Methodology

This strategy leverages 2 time frames analysis to have the high probability reversal setups on lower time frame in the direction of the 1D time frame trend. That’s why it’s recommended to use this strategy on 30 min – 4 hours time frames.

To have an approximation of 1D time frame trend strategy utilizes classical Stochastic indicator. The Stochastic Indicator is a momentum oscillator that compares a security's closing price to its price range over a specific period. It's used to identify overbought and oversold conditions. The indicator ranges from 0 to 100, with readings above 80 indicating overbought conditions and readings below 20 indicating oversold conditions.

It consists of two lines:

%K: The main line, calculated using the formula (CurrentClose−LowestLow)/(HighestHigh−LowestLow)×100 . Highest and lowest price taken for 14 periods.

%D: A smoothed moving average of %K, often used as a signal line.

Strategy logic assumes that on 1D time frame it’s uptrend in %K line is above the %D line. Moreover, we can consider long trade only in %K line is below 80. It means that in overbought state the long trade will not be opened due to higher probability of pullback or even major trend reversal. If these conditions are met we are going to our working (lower) time frame.

On the chosen time frame, we remind you that for correct work of this strategy you shall use 30min – 4h time frames, MACD line shall cross over it’s signal line. The MACD (Moving Average Convergence Divergence) is a popular momentum and trend-following indicator used in technical analysis. It helps traders identify changes in the strength, direction, momentum, and duration of a trend in a stock's price.

The MACD consists of three components:

MACD Line: This is the difference between a short-term Exponential Moving Average (EMA) and a long-term EMA, typically calculated as: MACD Line=12-period EMA−26-period

Signal Line: This is a 9-period EMA of the MACD Line, which helps to identify buy or sell signals. When the MACD Line crosses above the Signal Line, it can be a bullish signal (suggesting a buy); when it crosses below, it can be a bearish signal (suggesting a sell).

Histogram: The histogram shows the difference between the MACD Line and the Signal Line, visually representing the momentum of the trend. Positive histogram values indicate increasing bullish momentum, while negative values indicate increasing bearish momentum.

In our script we are interested in only MACD and signal lines. When MACD line crosses signal line there is a high chance that short-term trend reversed to the upside. We use this strategy on 45 min time frame.

ATR is used to adjust the strategy risk management to the current market volatility. If volatility is low, we don’t need the large stop loss to understand the there is a high probability that we made a mistake opening the trade. User can setup the settings ATR Stop Loss and ATR Trailing Profit Activation Level to realize his own risk to reward preferences, but the unique feature of a strategy is that after reaching trailing profit activation level strategy is trying to follow the trend until it is likely to be finished instead of using fixed risk management settings. It allows sometimes to be involved in the large movements.

Backtest Results

Operating window: Date range of backtests is 2023.01.01 - 2024.08.01. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 30%

Maximum Single Position Loss: -4.79%

Maximum Single Profit: +20.14%

Net Profit: +2361.33 USDT (+44.72%)

Total Trades: 123 (44.72% win rate)

Profit Factor: 1.623

Maximum Accumulated Loss: 695.80 USDT (-5.48%)

Average Profit per Trade: 19.20 USDT (+0.59%)

Average Trade Duration: 30 hours

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

How to Use

Add the script to favorites for easy access.

Apply to the desired timeframe between 30 min and 4 hours and chart (optimal performance observed on 45 min BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

Bollinger Bands Enhanced StrategyOverview

The common practice of using Bollinger bands is to use it for building mean reversion or squeeze momentum strategies. In the current script Bollinger Bands Enhanced Strategy we are trying to combine the strengths of both strategies types. It utilizes Bollinger Bands indicator to buy the local dip and activates trailing profit system after reaching the user given number of Average True Ranges (ATR). Also it uses 200 period EMA to filter trades only in the direction of a trend. Strategy can execute only long trades.

Unique Features

Trailing Profit System: Strategy uses user given number of ATR to activate trailing take profit. If price has already reached the trailing profit activation level, scrip will close long trade if price closes below Bollinger Bands middle line.

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Major Trend Filter: Strategy utilizes 100 period EMA to take trades only in the direction of a trend.

Flexible Risk Management: Users can choose number of ATR as a stop loss (by default = 1.75) for trades. This is flexible approach because ATR is recalculated on every candle, therefore stop-loss readjusted to the current volatility.

Methodology

First of all, script checks if currently price is above the 200-period exponential moving average EMA. EMA is used to establish the current trend. Script will take long trades on if this filtering system showing us the uptrend. Then the strategy executes the long trade if candle’s low below the lower Bollinger band. To calculate the middle Bollinger line, we use the standard 20-period simple moving average (SMA), lower band is calculated by the substruction from middle line the standard deviation multiplied by user given value (by default = 2).

When long trade executed, script places stop-loss at the price level below the entry price by user defined number of ATR (by default = 1.75). This stop-loss level recalculates at every candle while trade is open according to the current candle ATR value. Also strategy set the trailing profit activation level at the price above the position average price by user given number of ATR (by default = 2.25). It is also recalculated every candle according to ATR value. When price hit this level script plotted the triangle with the label “Strong Uptrend” and start trail the price at the middle Bollinger line. It also started to be plotted as a green line.

When price close below this trailing level script closes the long trade and search for the next trade opportunity.

Risk Management

The strategy employs a combined and flexible approach to risk management:

It allows positions to ride the trend as long as the price continues to move favorably, aiming to capture significant price movements. It features a user-defined ATR stop loss parameter to mitigate risks based on individual risk tolerance. By default, this stop-loss is set to a 1.75*ATR drop from the entry point, but it can be adjusted according to the trader's preferences.

There is no fixed take profit, but strategy allows user to define user the ATR trailing profit activation parameter. By default, this stop-loss is set to a 2.25*ATR growth from the entry point, but it can be adjusted according to the trader's preferences.

Justification of Methodology

This strategy leverages Bollinger bangs indicator to open long trades in the local dips. If price reached the lower band there is a high probability of bounce. Here is an issue: during the strong downtrend price can constantly goes down without any significant correction. That’s why we decided to use 200-period EMA as a trend filter to increase the probability of opening long trades during major uptrend only.

Usually, Bollinger Bands indicator is using for mean reversion or breakout strategies. Both of them have the disadvantages. The mean reversion buys the dip, but closes on the return to some mean value. Therefore, it usually misses the major trend moves. The breakout strategies usually have the issue with too high buy price because to have the breakout confirmation price shall break some price level. Therefore, in such strategies traders need to set the large stop-loss, which decreases potential reward to risk ratio.

In this strategy we are trying to combine the best features of both types of strategies. Script utilizes ate ATR to setup the stop-loss and trailing profit activation levels. ATR takes into account the current volatility. Therefore, when we setup stop-loss with the user-given number of ATR we increase the probability to decrease the number of false stop outs. The trailing profit concept is trying to add the beat feature from breakout strategies and increase probability to stay in trade while uptrend is developing. When price hit the trailing profit activation level, script started to trail the price with middle line if Bollinger bands indicator. Only when candle closes below the middle line script closes the long trade.

Backtest Results

Operating window: Date range of backtests is 2020.10.01 - 2024.07.01. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 30%

Maximum Single Position Loss: -9.78%

Maximum Single Profit: +25.62%

Net Profit: +6778.11 USDT (+67.78%)

Total Trades: 111 (48.65% win rate)

Profit Factor: 2.065

Maximum Accumulated Loss: 853.56 USDT (-6.60%)

Average Profit per Trade: 61.06 USDT (+1.62%)

Average Trade Duration: 76 hours

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

How to Use

Add the script to favorites for easy access.

Apply to the desired timeframe and chart (optimal performance observed on 4h BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

GKD-BT Multi-Ticker CC Backtest [Loxx]The Giga Kaleidoscope GKD-BT Multi-Ticker CC Backtest is a backtest module included in Loxx's "Giga Kaleidoscope Modularized Trading System."

█ Giga Kaleidoscope GKD-BT Multi-Ticker CC Backtest

This backtest allows you to test GKD-C Confirmation 1 and GKD-C Confirmation 2 indicators together without the hassle of adding additional confluence indicators. The backtest includes 1 take profit and 1 SL and various types of volatility. The backtest results on the chart are using 10% equity of 1 million total equity and $5 commission per trade.

To use this indicator:

1. Import the value "Input into NEW GKD-BT Backtest" from the GKD-C Confirmation 1 indicator into the GKD-BT Multi-Ticker CC Backtest.

2. Import the value "Input into NEW GKD-BT Backtest" from the GKD-C Confirmation 2 indicator into the GKD-BT Multi-Ticker CC Backtest.

This backtest includes the following metrics:

1. Net profit: Overall profit or loss achieved.

2. Total Closed Trades: Total number of closed trades, both winning and losing.

3. Total Percent Wins: Total wins, whether long or short, for the selected time interval regardless of commissions and other profit-modifying addons.

4. Percent Profitable: Total wins, whether long or short, that are also profitable, taking commissions into account.

5. Profit Factor: The ratio of gross profits to gross losses, indicating how much money the strategy made for every unit of money it lost.

6. Average Profit per Trade: The average gain or loss per trade, calculated by dividing the net profit by the total number of closed trades.

7. Average Number of Bars in Trade: The average number of bars that elapsed during trades for all closed trades.

Summary of notable settings:

Input Tickers separated by commas: Allows the user to input tickers separated by commas, specifying the symbols or tickers of financial instruments used in the backtest. The tickers should follow the format "EXCHANGE:TICKER" (e.g., "NASDAQ:AAPL, NYSE:MSFT").

Import GKD-B Baseline: Imports the "GKD-B Baseline" indicator.

Import GKD-V Volatility/Volume: Imports the "GKD-V Volatility/Volume" indicator.

Import GKD-C Confirmation: Imports the "GKD-C Confirmation" indicator.

Import GKD-C Continuation: Imports the "GKD-C Continuation" indicator.

Initial Capital: Represents the starting account balance for the backtest, denominated in the base currency of the trading account.

Order Size: Determines the quantity of contracts traded in each trade.

Order Type: Specifies the type of order used in the backtest, either "Contracts" or "% Equity."

Commission: Represents the commission per order or transaction cost incurred in each trade.

█ Giga Kaleidoscope Modularized Trading System

Core components of an NNFX algorithmic trading strategy

The NNFX algorithm is built on the principles of trend, momentum, and volatility. There are six core components in the NNFX trading algorithm:

1. Volatility - price volatility; e.g., Average True Range, True Range Double, Close-to-Close, etc.

2. Baseline - a moving average to identify price trend

3. Confirmation 1 - a technical indicator used to identify trends

4. Confirmation 2 - a technical indicator used to identify trends

5. Continuation - a technical indicator used to identify trends

6. Volatility/Volume - a technical indicator used to identify volatility/volume breakouts/breakdown

7. Exit - a technical indicator used to determine when a trend is exhausted

8. Metamorphosis - a technical indicator that produces a compound signal from the combination of other GKD indicators*

*(not part of the NNFX algorithm)

What is Volatility in the NNFX trading system?

In the NNFX (No Nonsense Forex) trading system, ATR (Average True Range) is typically used to measure the volatility of an asset. It is used as a part of the system to help determine the appropriate stop loss and take profit levels for a trade. ATR is calculated by taking the average of the true range values over a specified period.

True range is calculated as the maximum of the following values:

-Current high minus the current low

-Absolute value of the current high minus the previous close

-Absolute value of the current low minus the previous close

ATR is a dynamic indicator that changes with changes in volatility. As volatility increases, the value of ATR increases, and as volatility decreases, the value of ATR decreases. By using ATR in NNFX system, traders can adjust their stop loss and take profit levels according to the volatility of the asset being traded. This helps to ensure that the trade is given enough room to move, while also minimizing potential losses.

Other types of volatility include True Range Double (TRD), Close-to-Close, and Garman-Klass

What is a Baseline indicator?

The baseline is essentially a moving average, and is used to determine the overall direction of the market.

The baseline in the NNFX system is used to filter out trades that are not in line with the long-term trend of the market. The baseline is plotted on the chart along with other indicators, such as the Moving Average (MA), the Relative Strength Index (RSI), and the Average True Range (ATR).

Trades are only taken when the price is in the same direction as the baseline. For example, if the baseline is sloping upwards, only long trades are taken, and if the baseline is sloping downwards, only short trades are taken. This approach helps to ensure that trades are in line with the overall trend of the market, and reduces the risk of entering trades that are likely to fail.

By using a baseline in the NNFX system, traders can have a clear reference point for determining the overall trend of the market, and can make more informed trading decisions. The baseline helps to filter out noise and false signals, and ensures that trades are taken in the direction of the long-term trend.

What is a Confirmation indicator?

Confirmation indicators are technical indicators that are used to confirm the signals generated by primary indicators. Primary indicators are the core indicators used in the NNFX system, such as the Average True Range (ATR), the Moving Average (MA), and the Relative Strength Index (RSI).

The purpose of the confirmation indicators is to reduce false signals and improve the accuracy of the trading system. They are designed to confirm the signals generated by the primary indicators by providing additional information about the strength and direction of the trend.

Some examples of confirmation indicators that may be used in the NNFX system include the Bollinger Bands, the MACD (Moving Average Convergence Divergence), and the MACD Oscillator. These indicators can provide information about the volatility, momentum, and trend strength of the market, and can be used to confirm the signals generated by the primary indicators.

In the NNFX system, confirmation indicators are used in combination with primary indicators and other filters to create a trading system that is robust and reliable. By using multiple indicators to confirm trading signals, the system aims to reduce the risk of false signals and improve the overall profitability of the trades.

What is a Continuation indicator?

In the NNFX (No Nonsense Forex) trading system, a continuation indicator is a technical indicator that is used to confirm a current trend and predict that the trend is likely to continue in the same direction. A continuation indicator is typically used in conjunction with other indicators in the system, such as a baseline indicator, to provide a comprehensive trading strategy.

What is a Volatility/Volume indicator?